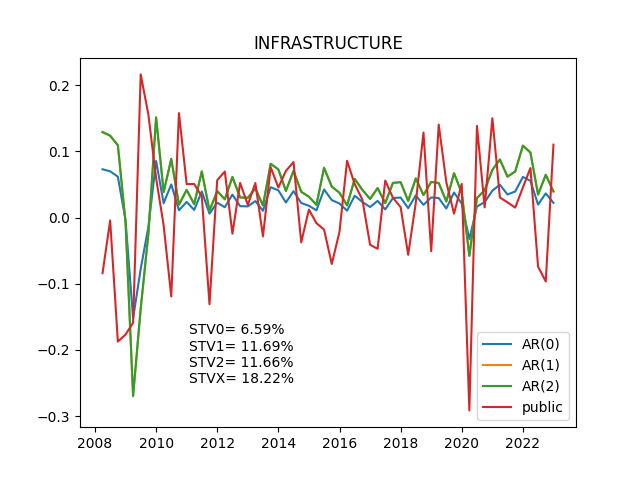

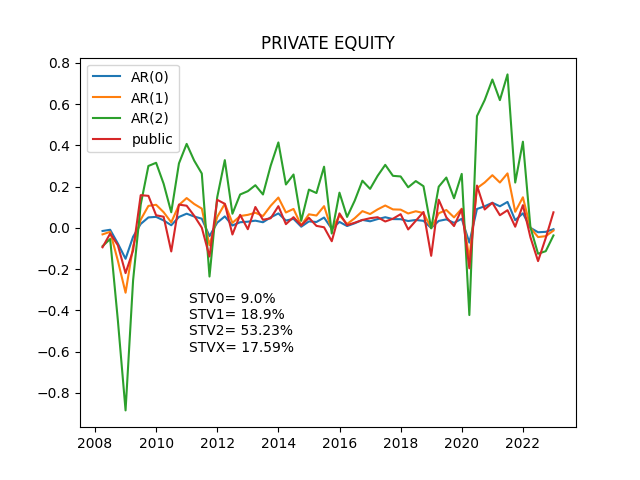

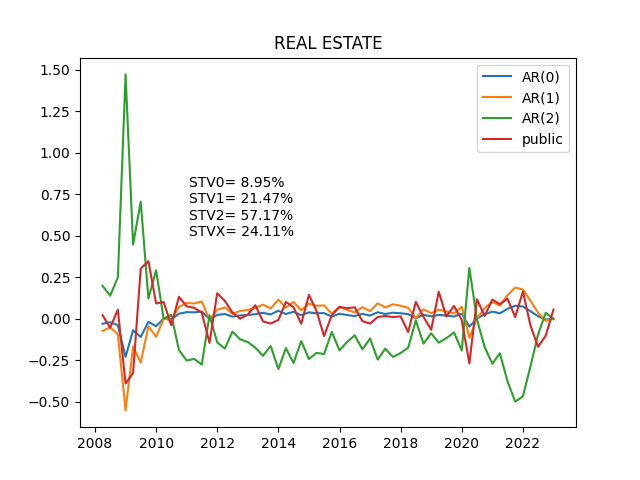

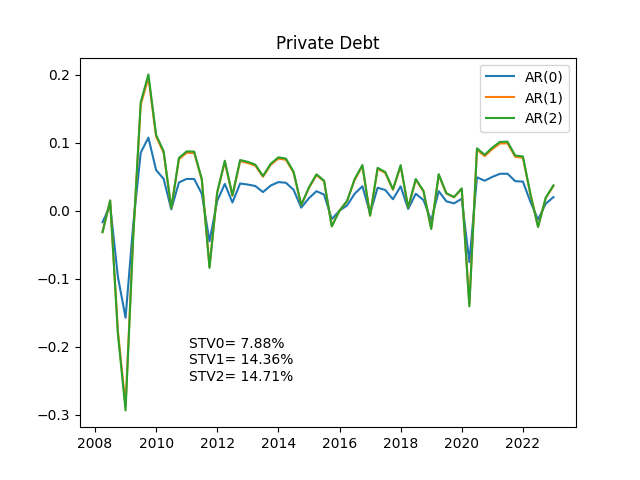

オルタナティブ分析(リターン複製)

<使用データ>

<コード>

import numpy as np

import pandas as pd

# 統計モデル

import statsmodels.api as sm

# from matplotlib import pylab as plt

from matplotlib import pyplot as plt

filepath = 'C:***********************************************************'

df = pd.read_csv(filepath + 'preqin_return202212_2.csv',dtype=str,usecols=['DATE','INFRASTRUCTURE','REAL ESTATE DEBT','PRIVATE EQUITY','REAL ESTATE','Private Debt','PUBRIC_US_STOCK','PUBRIC_US_REIT','PUBRIC_US_INFRA'],index_col='DATE',parse_dates=True)

alt_style = 'PRIVATE EQUITY'

#df['前日比%'] = df['前日比%'].astype('str')

df[alt_style] = df[alt_style].str.replace('%', '')

df[alt_style] = df[alt_style].astype(float)

df[alt_style] = df[alt_style]/100

pblic_style = 'PUBRIC_US_STOCK'

# 'PUBRIC_US_STOCK','PUBRIC_US_REIT','PUBRIC_US_INFRA'

df[pblic_style] = df[pblic_style].str.replace('%', '')

df[pblic_style] = df[pblic_style].astype(float)

df[pblic_style] = df[pblic_style]/100

# データセット確認

# print(df[alt_style])

# plt.plot(df[alt_style])

# plt.show()

# 自己相関を求める

df_acf = sm.tsa.stattools.acf(df[alt_style], nlags=30)

# 1期前

kei1=1-df_acf[1]

# 2期前

kei2=1-df_acf[1]-df_acf[2]

print(kei1)

print(kei2)

# データフレーム作成

newdf = pd.DataFrame(df[alt_style])

newdf['AR_1'] = df[alt_style]/kei1

newdf['AR_2'] = df[alt_style]/kei2

# 比較用上場インデックス組入れ

newdf['public'] = df[pblic_style]

sem0_df = np.std(df[alt_style])*2*100

sem1_df = np.std(newdf['AR_1'])*2*100

sem2_df = np.std(newdf['AR_2'])*2*100

semX_df = np.std(newdf['public'])*2*100

sem0_df = round(sem0_df,2)

sem1_df = round(sem1_df,2)

sem2_df = round(sem2_df,2)

semX_df = round(semX_df,2)

pltstr = 'STV0= ' + str(sem0_df) + '%'

pltstr = pltstr + '\n' + 'STV1= ' + str(sem1_df) + '%'

pltstr = pltstr + '\n' + 'STV2= ' + str(sem2_df) + '%'

pltstr = pltstr + '\n' + 'STVX= ' + str(semX_df) + '%'

# print(pltstr)

# リターングラフ

plt.title(alt_style)

plt.plot(newdf)

plt.legend(['AR(0)','AR(1)','AR(2)','public'])

x = 15000

y = -0.6

plt.text(x,y,pltstr,fontsize=10,color='black')

plt.show()